Global Healthcare Logistics Market Insights 2024: A $290.73

Dublin, July 25, 2024 (GLOBE NEWSWIRE) — The “Global Healthcare Logistics Market – Focused Insights 2024-2029” report has been added to ResearchAndMarkets.com’s offering.

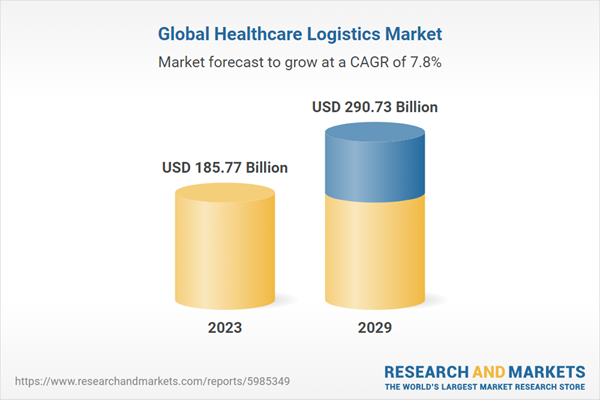

The Global Healthcare Logistics Market was valued at USD 185.77 billion in 2023, and is expected to reach USD 290.73 billion by 2029, rising at a CAGR of 7.75%.

The global healthcare logistics market report consists of exclusive data on 41 vendors. The global healthcare logistics market is highly fragmented and is classified by the presence of a few key vendors holding a majority of the share. The vendors offer logistics services in varied industries such as aerospace, consumer and retail, e-commerce, energy, automotive, healthcare, etc

The market is rapidly evolving in response to demand for faster deliveries by end users and increased visibility into shipments. Cencora, CEVA Logistics, Deutsch Post DHL, FedEx Corporation, Kuehne + Nagel, DB Schenker, and UPS are the key vendors in this market. These companies have a broad geographical footprint, a strong focus on innovation in logistics, and a diversified service portfolio.

The North American region dominates with the largest market share of over 34% in the global healthcare logistics market. This dominance is mainly due to the presence of the majority of healthcare suppliers in the region. High acceptance, prevalence of chronic disease, and growing geriatric population are some factors contributing to this region’s growth.

The APAC region shows significant global healthcare logistics market growth during the forecast period. The emerging Asian markets have garnered significant attention from the pharmaceutical industry due to their immense potential. The market is heavily influenced by government spending on research and development (R&D) and increasing health awareness, particularly in emerging markets like India and China. Factors such as the proportion of the senior population (aged 65 years and above) and the rising life expectancy have significantly contributed to creating new business opportunities for the pharmaceutical industry across the APAC region.

MARKET TRENDS & DRIVERS

Optimizing Healthcare Supply Chain Through Digital Transformation

In recent years, the healthcare industry has increasingly turned to digital transformation to address the challenges and complexities of supply chain management. Healthcare organizations can unlock numerous benefits and efficiencies throughout the supply chain process by integrating advanced technologies into their operations. One key aspect of digital transformation in healthcare supply chains is adopting advanced analytics and artificial intelligence (AI).

These technologies enable organizations to analyze vast amounts of real-time data, identify patterns and trends, and make data-driven decisions. For example, AI-powered predictive analytics can help forecast demand for medical supplies, allowing organizations to optimize inventory levels and prevent stockouts or overstocking. Blockchain provides a secure and transparent way to track and trace products throughout the supply chain. The Internet of Things (IoT) plays a significant role in digitalizing healthcare supply chains. IoT devices such as RFID tags and sensors can be attached to medical supplies, equipment, and patients to monitor their location, condition, and usage in real-time.

M&A Strategies Expanding Healthcare into Non-Acute Settings

The shift towards non-acute care settings represents a fundamental transformation in healthcare delivery, driven by the need to improve access, reduce costs, and enhance patient outcomes. Ambulatory surgery centers, community clinics, and home care services offer more convenient and less expensive alternatives to traditional hospital-based care, particularly for routine procedures and chronic disease management.

Mergers and acquisitions are significant in this transition as healthcare organizations seek to expand their reach and capabilities by integrating non-acute services into their networks. For example, a health system may acquire a local hospital that operates ambulatory surgery centers or a network of clinics, allowing for better coordination of care and improved patient access across the continuum.

The move towards non-acute care settings and preventative care reflects a broader shift towards value-based healthcare models prioritizing patient-centered, holistic wellness approaches. Through strategic M&A activities and targeted initiatives, healthcare organizations aim to create more efficient, equitable, and sustainable healthcare systems that meet the diverse needs of patients and communities.

Adoption of Cloud-based Enterprise Resource Planning (ERP) Systems

Adopting cloud-based enterprise resource planning (ERP) systems in the healthcare supply chain has significantly improved data management practices. These systems serve as centralized hubs for storing and managing vast amounts of data related to inventory, procurement, distribution, and other supply chain activities. One of the key benefits of cloud-based ERP systems is their ability to integrate data from various sources into a single, unified platform. This integration facilitates real-time visibility into inventory levels, demand patterns, and supply chain performance metrics across multiple facilities and locations. With all relevant data accessible from a centralized location, supply chain managers can make informed decisions quickly and efficiently.

Furthermore, cloud-based ERP systems enable the deployment of advanced technologies such as artificial intelligence (AI) and machine learning (ML). These technologies leverage the rich data stored in the ERP system to drive predictive analytics and optimization algorithms. For example, AI and ML algorithms can analyze historical demand patterns to forecast future inventory needs more accurately, helping organizations optimize stock levels and reduce the risk of stockouts or excess inventory.

Moreover, AI-powered analytics can identify potential disruptions in the supply chain, such as delays in product delivery or fluctuations in demand, allowing supply chain managers to address these issues before they escalate proactively. By leveraging AI-driven insights, healthcare organizations can improve supply chain resilience, minimize risks, and enhance operational efficiency.

INDUSTRY RESTRAINTS

Supply and Equipment Shortages

In the healthcare industry, supply-chain challenges persistently plague providers, hindering their access to essential supplies and equipment. These challenges, initially heightened by the disruptions caused by the COVID-19 pandemic, continue to reverberate, affecting routine and pandemic-related items. Despite concerted efforts to maintain adequate stock levels, healthcare providers struggle to balance product availability, timely delivery, cost-effectiveness, and appropriate measurement units.

Surveys conducted in 2023 indicate that supplier shortages remain pervasive, with over 90% of providers grappling with ongoing difficulties obtaining critical supplies. These shortages have profound implications for healthcare delivery, impacting patient care, operational efficiency, and overall healthcare system resilience. Healthcare providers must navigate an uncertain landscape, seeking alternative sourcing strategies, optimizing inventory management practices, and collaborating closely with suppliers to mitigate supply-chain disruptions.

SEGMENT ANALYSIS

INSIGHT BY PRODUCT TYPE

The global healthcare logistics market by product type is segmented into pharmaceuticals and medical devices. The pharmaceuticals segment will dominate with the largest market share in 2023. The growth can be attributed to the increasing healthcare expenditure, a surge in R&D investments, and the emergence of biologics and biosimilars.

Pharmaceutical supply chain management involves strategically coordinating the complete value-added process of a product within the pharmaceutical industry, along with its associated logistics. This encompasses collaborative efforts among manufacturers, suppliers, distributors, business partners, and consumers, from procurement to final delivery.

INSIGHT BY FUNCTIONALITY TYPE

The global healthcare logistics market by functionality is categorized into transportation (road, water, air), warehousing, etc. The air transportation segment shows prominent growth, with the fastest-growing CAGR during the forecast period. Air freight has emerged as a vital component of the global economy, enabling swift and efficient transportation of goods worldwide, thus helping segmental growth.

While air transport has historically been the pharmaceutical industry’s favored choice for international shipping due to its unparalleled speed and adaptability, a notable shift is occurring as more industry leaders turn their attention to ocean freight as a preferable alternative. The economic appeal is substantial, with air freight costing four times more than surface shipping. This shift is particularly compelling considering regulatory pressures from health authorities, which drive suppliers to reduce costs aggressively.

INSIGHT BY END-USER TYPE

The pharmacies segment holds the largest global healthcare logistics market share by end-user. The segmental growth is because pharmacies or drugstores are places where the medicines are dispensed or compounded. The pharmacists are responsible for the composition of the dosage forms of drugs, such as sterile solutions for injections, capsules, and tablets.

As the pharmaceutical industry grows, pharmacists emerge as trusted professionals, fueled by promising technologies and trends highlighted in recent forecast reports, with a focus on sustainability and development; health system pharmacists play a pivotal role, supported by advancements in communication technology and risk management under supply chain management, all aimed at enhancing patient healthcare systems.

KEY QUESTIONS ANSWERED

- What are the key trends in the global healthcare logistics market?

- Which region dominates the global healthcare logistics market?

- How big is the global healthcare logistics market?

- Who are the major players in the global healthcare logistics market?

- What is the growth rate of the global healthcare logistics market?

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 146 |

| Forecast Period | 2023 – 2029 |

| Estimated Market Value (USD) in 2023 | $185.77 Billion |

| Forecasted Market Value (USD) by 2029 | $290.73 Billion |

| Compound Annual Growth Rate | 7.7% |

| Regions Covered | Global |

Key Vendors

- Cencora

- CEVA Logistics

- FedEx

- Kuehne + Nagel

- DB Schenker

- Deutsche Post DHL Group

- United Parcel Service (UPS)

Other Prominent Vendors

- AWL

- Alloga

- Bollore Logistics

- Cardinal Health

- C.H. Robinson

- Cold Chain Technologies (CCT)

- DSV

- Farmasoft

- Lufthansa Cargo

- Medline

- Nippon Express Co. Ltd

- Oximio

- SEKO Logistics

- Sinotrans Limited

- XPO Logistics

- ZirconMed

- GXO

- ArcBest

- Associated Couriers

- Carousel Logistics

- Crane Worldwide Logistics

- CRYOPDP

- DACHSER

- Expeditors

- Freight Logistics Solutions

- Global Group

- Kenco

- Kerry Logistics Network

- Kintetsu World Express

- Life Science Logistics

- Mercury

- Nissin International Logistics Provider

- Rhenus Logistics

- Geodis

GEOGRAPHICAL ANALYSIS

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Spain

APAC

- Japan

- China

- India

- Australia

- South Korea

Latin America

Middle East & Africa

- Turkey

- South Africa

- Saudi Arabia

For more information about this report visit

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

- Global Healthcare Logistics Market

link